Ron

Ron

Sometimes you look like a genius when you do simple things. My neighbour Ravi investing for his son’s post-secondary education is one such example. Ravi started an education investment account for his son when he was born and managed to amass $40,000 by the time his son turned 6. Here is the interesting fact: if he has a total of 40k when his son is 6 years old, how much is he going to have invested when his son is 18 and ready to attend a college or university? A lot. A lot to get his son started financially as a student and further into his adult life.

As we all know, the cost of post-secondary education is increasing every year. Many students are graduating with high debt in a tough job market. Some are forced to work part-time to pay for education when they should be immersing in studies or getting the best out of college life. Upon graduation, if they are lucky enough to find the right job, they will have to start servicing their debt. Servicing debt at an early age will deprive them of income that can be used for other purposes including saving and investing for the future. Can parents help? Yes, they can with some planning and some effort. Here’s how based on Ravi’ approach:

After sweating it out in the birthing unit when his son was born, Ravi started an RESP account for his son at the bank. RESP stands for Registered Education Saving Plan and it is an investment account to save for children’s education for Canadians. The plan consists of the following:

1. Parents can contribute up to 50k into the plan over the lifetime of the child.

2. The government matches the contribution up to 20% (to a maximum of $500 per year) and even more for modest income families. This is a smart plan by the government as a skilled workforce is in the nation’s best interest.

3. You can invest in any financial products anywhere from conservative GICs to riskier stocks.

4. Tax is paid on withdrawal at the hands of the student. A 20% penalty is imposed on any amount withdrawn for non-educational expenses.

Ravi, who believes in low-cost mutual funds for passive investments like an RESP, opened an account and picked TD e-series to create a portfolio as follows:

- TD E-series Canadian Index (30% allocation)

- TD E-series US Index (30% allocation)

- TD E-series International Index (30% allocation)

- TD E-series Canadian Bond Index (10% allocation)

The above portfolio consists of major stocks from all over the world with a fee (MER) lower than 0.5%. Ravi setup a monthly contribution (also called Dollar Cost Averaging) and set-up a $330 automatic contribution into this account ($330 would be automatically taken out of his account every month and invested in this portfolio). He did not look frequently into how his portfolio performed as he believed that over time he will get a good return. Instead he watched his son grow from a baby to a toddler to a 6 year old young man; he changed his diapers, taught him to ride a bike, played Wii and cherished every moment he spent with him.

As for the portfolio, the only thing he did was to rebalance it once every year. So if any of above funds went over the allocated percentage, he would bring it back to the target allocation of 30% and 10%. This is a widely practiced method of investing and is called Couch Potato strategy.

Ravi looked at the portfolio on his son’s 6th birthday, and thanks to a well-performing market and the magic of compounding, the balance had ballooned to 40k. How much will the RESP balance be 12 years from now when his son will be 18?

If we assume a continued monthly contributions of $330 up to 50k, a 9.5% average return (7% return on the contribution and 1.5% extra return based on the government matching), he will have about 155k which is more than enough for a 4 year degree. His son can choose to spend the rest for graduate studies or in any other productive way.

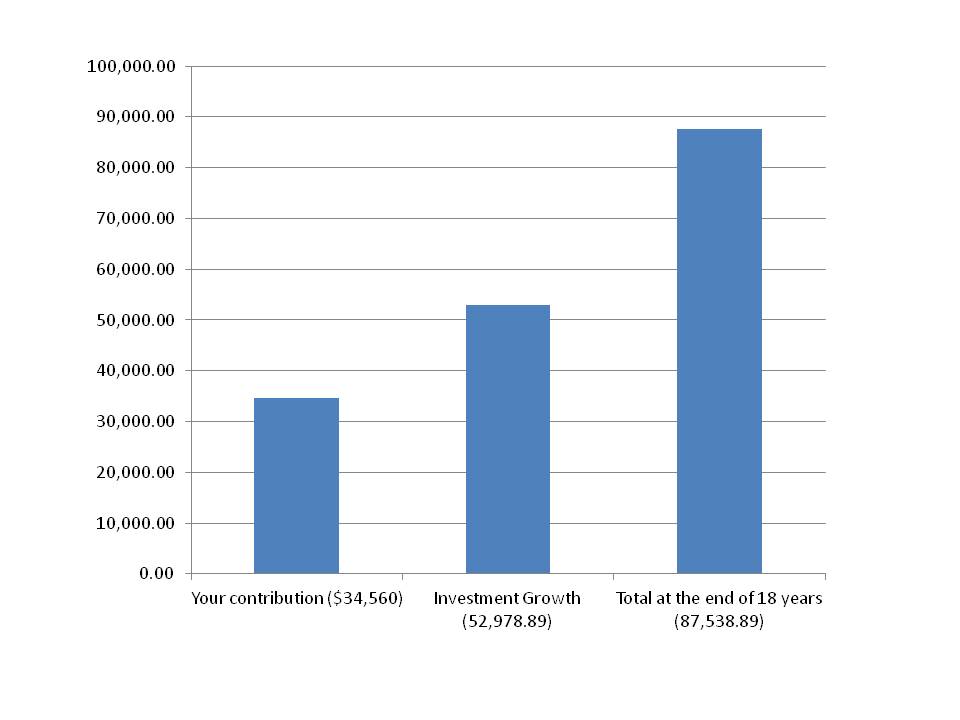

Not every one of us can afford to contribute $330 monthly for a child with all the expenses associated with raising one or more children. How about if we choose to contribute $160 every month instead? The investment will turn to 87K in 18 years assuming the same return as above. That will still be more than enough for a 4 year post-secondary education in the future.

RESP return based on a monthly contribution of $160 for 18 years

This investment strategy is simple and followed by DIY (Do-it-yourself) investors. Alternatively, you can use the financial firms that provide RESP investment services. Find the right one and make sure they keep your interest in mind when working with you. If you are risk averse, you can avoid stocks completely or partly and go for conservative investments like GICs which will provide lower returns at less risk. You can also employ other strategies like taking a higher risk at a young age and lower risk later.

As a community, we value education and this is a small thing we can do for the next generation. Remember to do this before organizing that expensive, Tamil-style first year birthday bash for your child!

More From This Author:

Ananda Krishnan: The Richest Tamil in the World

10 Tips on Investing for the Future from My Wealthy Neighbour

The Tamil Millionaire Next Door

Featured image sourced from VisaPro.